D

DerDaily

April 11, 2026

The developer is great and creates excellent products. If possible, adding red folders and date/time/countdown/exc details would be a nice bonus. Overall, it’s flawless work.

Real-time ES/NQ futures quality terminal: 6-pillar composite score, directional bias, and position sizing in one dashboard

$7.50/mo

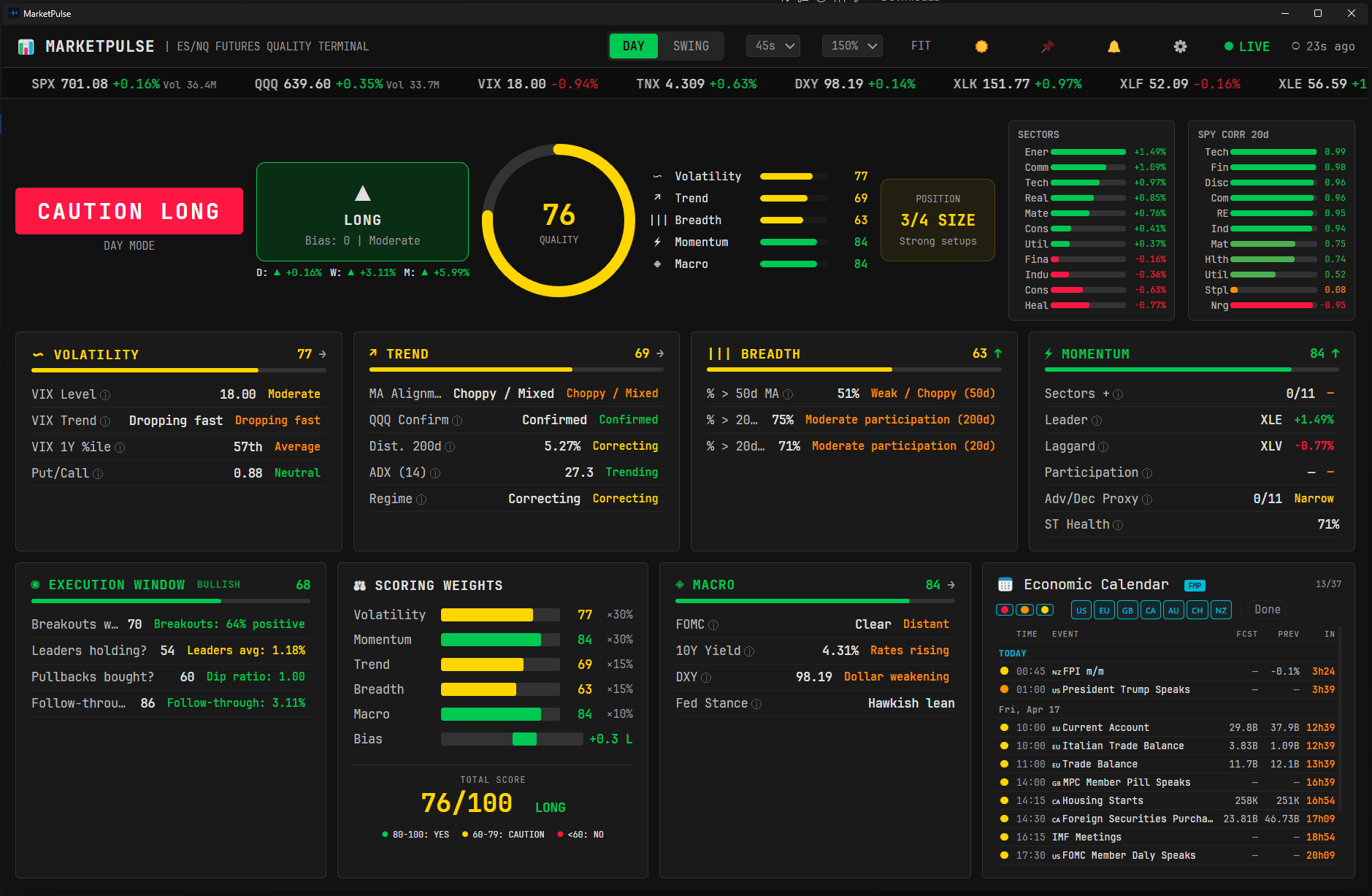

Volatility, Momentum, Trend, Breadth, Macro, and Execution weighted into a single 0-100 composite score. Answers: "Should I trade today?"

LONG/SHORT/NEUTRAL with strength indicator, multi-timeframe alignment (D/W/M), and automatic position sizing recommendation (FULL to FLAT).

Standalone .exe. No API key, no Python, no database. Double-click and get a Bloomberg-style terminal with live market data in 30 seconds.

Market Pulse is a real-time market quality terminal for ES (S&P 500) and NQ (Nasdaq 100) futures traders. It aggregates six analytical pillars (Volatility, Momentum, Trend, Breadth, Macro, and Execution) into a single composite score from 0 to 100, a directional bias (LONG / SHORT / NEUTRAL), and a recommended position size (FULL to FLAT).

The interface is inspired by professional trading terminals: dark background, monospace typography, semantic color coding (green = favorable, red = risk, yellow = caution), and a dense but readable layout.

Market Pulse answers two fundamental questions before every session:

| Question | Answer |

|---|---|

| Should I trade today? | The composite score: YES (80+), CAUTION (60-79), or NO (<60) |

| In which direction? | The directional bias: LONG, SHORT, or NEUTRAL |

A high score does not mean the market is going up: it means conditions are favorable for trading. A strong downtrend with clear breadth alignment and low VIX can score 90+, signaling excellent conditions for short trades.

Evaluates the volatility environment. Combines VIX level, 5-day slope, 1-year percentile, and estimated Put/Call ratio. Low and stable VIX = best conditions.

Measures price momentum quality (direction-agnostic). Uses RSI 14d with smoothed scoring (continuous interpolation, no discontinuous jumps), 5d/20d absolute returns, sector leader/laggard participation, and an Advance/Decline proxy with Short-Term Health reading. Strong momentum in any direction = high quality.

Assesses trend clarity via moving average alignment (Bullish/Bearish Stack detection), QQQ confirmation, distance to SMA 200d, and ADX (14) regime classification (±10 point bonus/malus). Clear trends = high quality, chop = low quality.

Measures market participation across 51 large-caps representing all 11 GICS sectors. Tracks % above SMA 20d, 50d, and 200d. Direction-agnostic: both strong participation (>75%) and washout (<25%) signal consensus = high quality.

Evaluates the macroeconomic backdrop: 10Y yield trend (TNX), dollar trend (DXY), and proximity to high-impact events (FOMC, CPI, NFP). Distant events + stable rates = favorable.

Adaptive pillar that checks whether setups in the dominant direction are actually working. Tracks breakdowns holding, laggards staying down (or leaders extending), bounce failures, and follow-through quality. Adjusts its metrics based on the current regime.

| Mode | Best for | Weighting emphasis |

|---|---|---|

| DAY | Intraday scalps and day trades | Volatility 30%, Momentum 30%, Trend 15%, Breadth 15%, Macro 10% |

| SWING | Multi-day positions | Volatility 25%, Momentum 25%, Trend 20%, Breadth 20%, Macro 10% |

Toggle between modes with the DAY/SWING button or keyboard shortcuts (D / S).

Based on the composite score, Market Pulse recommends a position size:

| Score | Size | Meaning |

|---|---|---|

| 80+ | FULL | Lean into risk |

| 70-79 | 3/4 | Solid setups |

| 60-69 | HALF | A+ setups only |

| 50-59 | QUARTER | Very selective |

| <50 | FLAT | Preserve capital |

A full week-ahead economic calendar lives at the bottom of the dashboard. Events are fetched from Forex Factory (free, no API key required) and ordered chronologically across the current trading week.

Three interactive chip rows let you narrow the calendar live:

Haut / Moyen / Bas) that mirror the red/orange/yellow dots next to every event. Click to include or exclude each impact tier. Combine freely (e.g. High + Low only).All filter states persist across app restarts.

Every upcoming event shows a 1-second countdown to release (03h 14m 22s). Imminent events (< 5 minutes) blink red; events within an hour are highlighted in orange. The countdown runs locally so it ticks smoothly without waiting for the next poll.

Each row displays the market Forecast and Previous value out of the box. For Actual values as they release, add a free Financial Modeling Prep API key in the Settings modal (250 free requests/day is more than enough for day trading). When the key is active, a small FMP badge appears in the calendar header and actual values populate live as they publish.

Two alert types, both delivered as native Windows notifications:

N minutes before a High-impact event (configurable in Settings: Disabled / 5 / 10 / 15 / 30 / 60 min, default 15). Tracked per event so an alert never fires twice.economic_calendar endpoint as a secondary source.A gear icon in the top bar opens a Settings overlay with three groups:

Disabled to silence only the pre-event alert while keeping decision/bias and on-release notifications active.Every change auto-saves to userData/settings.json, with no Save button.

Ctrl+R manual refreshT shortcut, ideal for multi-monitor trading desksD / S mode toggle, Ctrl+R refresh, T always-on-top, Delete minimize| Data | Source | Cadence |

|---|---|---|

| Prices + volume (SPY, QQQ, VIX, TNX, DXY, 11 sectors) | Yahoo Finance | Spot 60 s, history 8 h |

| 1-year daily OHLC | Yahoo Finance | 8 h |

| Breadth (51 large-caps) | Yahoo Finance | 8 h |

| FOMC / CPI / NFP proximity | Federal Reserve + BLS (scrape) | 12 h |

| Week-ahead economic events | Forex Factory (free, no key) | 5 min memory + 30 min disk |

| Actual values for economic events | FMP (optional, free key) | 2 min |

| Earnings (30 mega-caps) | Yahoo Finance | 12 h |

No data ever leaves your machine except the outbound API polls listed above. No telemetry, no account, no subscription to external platforms.

| Requirement | Specification |

|---|---|

| OS | Windows 10/11 (64-bit) |

| Internet | Required (live market data) |

| Disk space | ~150 MB |

| Display | 1920x1080 recommended |

| Installation | None: double-click market-pulse.exe |

| API keys | None required (FMP optional, free tier) |

| Dependencies | None, fully standalone |

DerDaily

April 11, 2026

The developer is great and creates excellent products. If possible, adding red folders and date/time/countdown/exc details would be a nice bonus. Overall, it’s flawless work.